In Cube’s recent commentary on Sea Limited’s Q1’26 earnings, one point that stood out was that Shopee VIP is beginning to look more Amazon Prime-like. VIP is no longer just about shopping discounts or shipping perks. It is becoming a broader membership layer, with lifestyle and non-shopping benefits increasingly used to deepen buyer engagement. It is a meaningful step forward, but it raises a frequently asked question among observers: how Amazon-like can Shopee actually become?

The answer, in our view, is nuanced. Shopee is clearly adopting several Amazon-like monetization levers: a paid membership layer, a growing ads business, a logistics layer around the marketplace, and a steady increase in seller-side fees. But adopting the same levers does not mean reaching the same endpoint.

Shopee has often been touted as Southeast Asia’s Amazon. It dominates regional e-commerce the way Amazon dominates the US, runs an in-house logistics layer like Fulfillment by Amazon (FBA), and is now building an ad business inside the marketplace.

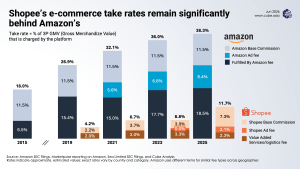

But these similarities do not appear to apply to the two platforms’ ability to monetize these investments. Amazon’s estimated 3P take rate (different from the overall take rate) – the percentage of revenue a marketplace platform takes from its third-party sellers has more than doubled from 18% in 2015 to 38% in 2025. Shopee’s comparable marketplace take rate has gone from 2% in 2018 to 12% in Q1 2026. The shape of the curve in both cases is upward, but the destination, we believe, will not converge.

Both platforms are currently charging three broad kinds of fees –

- Category-based commission/referral fee

- Ad fee

- Logistics and fulfillment-related fee

| Fee type | Amazon | Shopee |

| Category-based commission/referral fee | Fixed between 8 to 15% and has barely moved in a decade |

Increased 4x since 2018 from 2% to 8%. It bundles transaction-based fee, platform fees, and infrastructure fees in different markets Can expect this to increase, but at a much slower pace. |

| Ad take rate |

For many serious sellers on Amazon, advertising has become functionally unavoidable. Most of the best-converting screen space is allocated to advertising; thus, sellers inevitably have to advertise to have a chance to be discovered. In 2025, ~8% of Amazon’s take rate came from ads, up from 3% in 2020. |

Advertising on Shopee is becoming increasingly unavoidable. But even in the medium to long term, the management expects it to grow up to 4-5%. |

| Logistics and fulfillment-related fee |

FBA has the biggest share in the take rate. This cost has increased nearly every year through hikes for logistics and shipping. As faster delivery became the norm, FBA became the default for most sellers. |

Shopee charges a logistics fee but has been heavily subsidizing this to be price-competitive. What they get to keep shrinks even when the fulfillment volume and revenue grow. |

Three things bring out these differences –

1/ Higher Average Order Values – E-commerce AOVs across Southeast Asia remain much lower than in Amazon’s core US market. That gap is not just smaller wallets. It reflects a shopping pattern dominated by frequent, low-ticket purchases, increasingly fueled by live commerce and gamified vouchers.

This makes a structural difference for monetization: Even small commission or ad rate increases compress seller economics faster than they would in the US, which limits how aggressively Shopee can push the levers Amazon pushed.

2/ Less intense competition – Shopee leads in most SEA markets, but the competitive set is more crowded. TikTok Shop is consistently growing, and there’s always competition from local cross-border platforms with low price floors. Amazon raised FBA fees year after year in part because sellers had nowhere else to go at scale.

It is not unlikely that Shopee can exert a strong market leadership too, eventually, but possibly not to the same extent.

3/ Longer time horizon training both buyers and sellers – Amazon has spent over 20 years training US consumers to view free 2-day shipping not as a perk, but as a baseline utility. That’s a long horizon of behavioral training on both sides of the network. This forces sellers to use FBA to stay competitive.

Shopee’s buyer base is still accustomed to expecting specific service standards, and many SEA shoppers continue to optimise for price over speed, especially in cash-on-delivery markets. Shopee VIP is in the early days, and sellers, similarly, are still being formalised.

Even Amazon itself has shown that the Amazon model does not travel uniformly. Earlier in May, it wound down local fulfillment in Singapore. Clearly, a model that worked elsewhere in the world does not guarantee success in SE Asia.

In an optimistic scenario, Shopee’s 3P take rate could climb toward 18-22% by 2030. That would still be a major profit pool if GMV keeps compounding quickly. It is more likely, though, as a base case, that the take-rate will be in the 15-18% range by then.

It is visible in the layers of the chart below that it’s not simply a timing gap between the two platforms. Amazon’s economics were transformed by FBA and ads, becoming almost unavoidable for serious sellers. Shopee can borrow from the same playbook, but Southeast Asia’s lower AOVs, tougher competition, and more price-sensitive shoppers likely create a lower ceiling.