The e-commerce landscape in SEA is tightening. E-commerce Consolidation in SEA isn’t a prediction anymore; it’s the new reality. We’re seeing it play out in massive strategic alliances, like TikTok investing $1.5 billion for a 75.01% controlling stake in Tokopedia in Indonesia, and in the strengthening dominance of regional players like Shopee and Grab.

The “cash burn” era of wild growth is over. But here’s the problem: many brands are still stuck in the old playbook, fighting a price war.

The truth is, the battlefield has shifted. In this new consolidated era, the winner isn’t the brand with the biggest discount. It’s the brand that’s smartest with data right down to the most granular SKU (Stock Keeping Unit) level.

In this analysis, we’ll explore exactly why this shift is happening: from the rise of the ‘Super App Effect’ to the dangerous ‘Profit Squeeze’ on brands, and (most importantly) why the ‘Data’ is now the only way to win.

The Super App Effect: How Platform Loyalty is Killing Brand Loyalty

Consolidation is creating the “Super App” , a closed digital ecosystem where consumers can do everything, from shopping and paying bills to booking transport.

Shopee, Grab, and the GoTo/TikTok have evolved beyond just ecommerce but becoming the ‘digital worlds’ where consumers spend their time. This changes everything, because consumer loyalty is shifting. They’re no longer loyal to your brand, they’re loyal to the platform’s convenience and ecosystem.

This ‘stickiness’ is driven by more than just variety. It’s driven by deep, structural integration. In Southeast Asia, these Super Apps have successfully merged social, commerce, and (most critically) payments.

When a consumer’s digital wallet (like ShopeePay, GoPay, or GrabPay) is becoming the default payment method within the ecosystem, the friction to purchase drops to almost zero. This creates a powerful ‘walled garden’, where platforms are not just competing for consumer attention, they’re competing to own the entire purchasing journey.

This ecosystem lock makes pulling customers out to a brand’s own D2C (Direct-to-Consumer) website harder and more expensive than ever.

For brands, this means one thing: the battle must be won inside the app. So, in-app strategies like engaging live shopping programs which are proven to drive high conversion rates and 40% fewer product returns, and aggressive affiliate schemes now influencing an estimated 10-20% of total GMV, aren’t optional anymore. They’re an absolute necessity just to get noticed.

The Profit Squeeze: Responding to Rising Platform ‘Take-Rates’

After winning market share, these platform giants are unsurprisingly shifting their focus from “growth” to “profitability.”

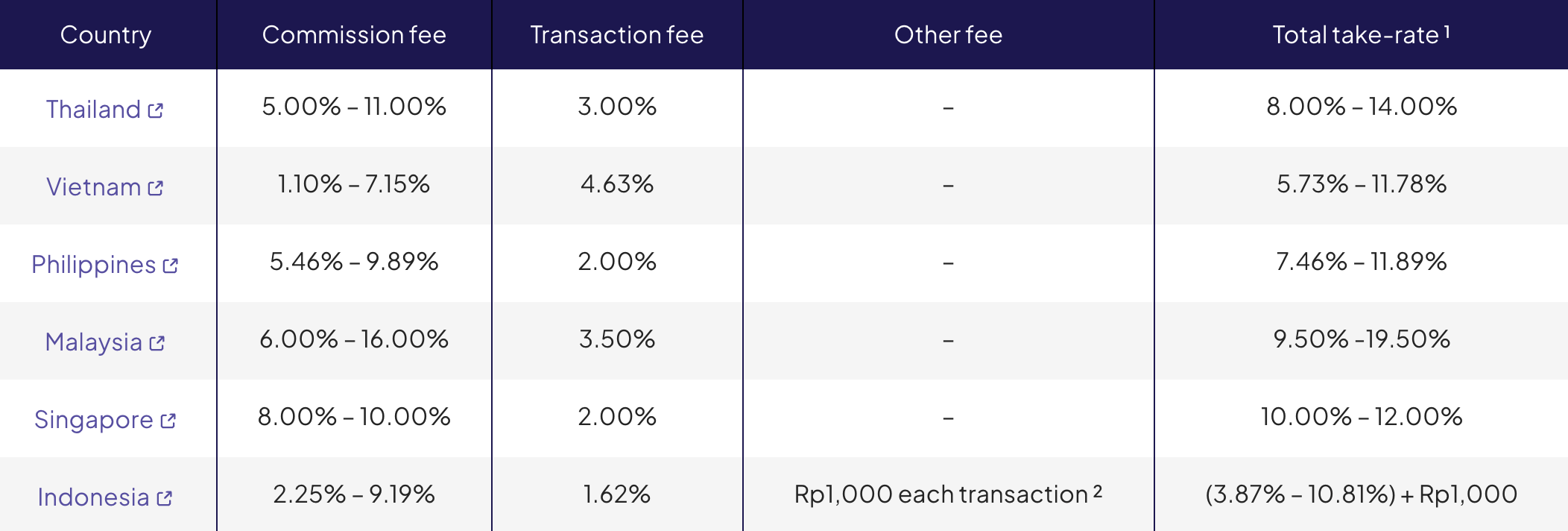

What’s this mean for your brand? Rising costs. Platforms are now aggressively jacking up commission fees, admin fees, and ad costs, what we track as the take-rate.

And we track this closely in our Take-Rate Tracker. Just look at our February 2025 data: the total take-rate (commission and transaction fees) for Shopee Mall in Malaysia can hit a staggering 19.5% for categories like fashion. And it’s climbing in other major markets, too.

This cost hike, combined with new e-commerce tax regulations like Indonesia’s 12% VAT increase, is squeezing brand margins. It’s a ‘one-two punch’ (the profit squeeze) that makes every single dollar in your budget count.

Let’s put that 19.5% Take-Rate into perspective. For every $100 in revenue a brand makes, $19.50 goes directly to the platform before the brand even pays for the product itself, marketing, or shipping. Add the 12% VAT, and the pressure becomes immense.

This fundamentally changes a brand’s inventory strategy. You can’t afford to stock slow moving SKUs. Every product listing must justify its place. This is why a “wait and see” approach isn’t viable, brands must be proactive.

Image 1. The Squeeze: Total Take-Rate (Shopee Mall, Feb 2025)

The Data War: Why Granular SKU Insights Now Beat Big Discounts

Because of this ‘one-two punch’, brands can’t just throw discounts at the wall anymore. A 50% blanket discount is a suicidal strategy in 2026. Your margins won’t survive.

This new era demands precision. The war has officially shifted from “price” to “data”.

You need to know: Which SKU (product variant) is actually selling best? Which competitor SKU is about to go out-of-stock? What discount strategy is your rival using for their hero SKU?

Let’s walk through a scenario: Brand A experienced a total sales drop. Their response by giving 50% blanket discount on all serum. At the end, it destroy their profit margin on their hero SKU (which would have sold anyway) and still fail to move their slow moving SKUs (which were being beaten by a competitor on features, not just price).

On the other hand, Brand B who saw the same thing, but leveraged their SKU level data. The data shows that sales drop wasn’t due to price, but because their hero SKU (50ml bottle) went out-of-stock for two weeks. Also, the 15ml SKU is being outsold by a rival’s new product. The possible strategy is by restocking the hero SKU (at full price), while discounting only the 15ml SKU to counter the competitor. They win, and their margins are protected.

Bottom line, you need granular competitive insights that let brands analyze competitor product rankings and develop actionable insights at the SKU level.

The Future is Granular

E-commerce consolidation in SEA is a fact. It’s creating ‘walled gardens’ controlled by Super Apps, and they’re squeezing brand margins at the same time.

In our perspective, guesswork is the most expensive strategy you can possibly have.

The winners will be the brands that react fastest to market trends, optimize profitability on every single SKU, and understand their competitors’ moves at the most detailed level. The price war might be over, but the data war has just begun.